All Categories

Featured

Table of Contents

There is no payment if the policy expires prior to your fatality or you live beyond the plan term. You may be able to renew a term plan at expiry, but the premiums will certainly be recalculated based on your age at the time of revival. Term life insurance policy is typically the the very least expensive life insurance coverage readily available because it provides a survivor benefit for a restricted time and does not have a cash money value component like permanent insurance.

At age 50, the costs would climb to $67 a month. Term Life Insurance Rates 30 years old $18 $15 40 years old $28 $23 50 years old $67 $51 Source: Quotacy. Quotes are for a $250,000 30-year term life plan, for males and women in outstanding health.

Which Of The Following Is Not A Characteristic Of Term Life Insurance

Interest rates, the financials of the insurance business, and state guidelines can likewise affect premiums. When you consider the amount of coverage you can obtain for your premium bucks, term life insurance policy has a tendency to be the least pricey life insurance.

Thirty-year-old George intends to shield his family members in the unlikely occasion of his passing. He buys a 10-year, $500,000 term life insurance policy plan with a premium of $50 per month. If George dies within the 10-year term, the policy will pay George's beneficiary $500,000. If he dies after the plan has actually ended, his beneficiary will obtain no advantage.

If George is identified with an incurable illness throughout the very first policy term, he probably will not be qualified to restore the policy when it expires. Some plans supply guaranteed re-insurability (without proof of insurability), but such features come at a greater price. There are several sorts of term life insurance policy.

Most term life insurance coverage has a level costs, and it's the type we have actually been referring to in most of this post.

What Is Level Benefit Term Life Insurance

Term life insurance coverage is appealing to youngsters with kids. Moms and dads can get considerable protection for an affordable, and if the insured dies while the policy holds, the family can depend on the survivor benefit to replace lost earnings. These policies are also well-suited for individuals with growing households.

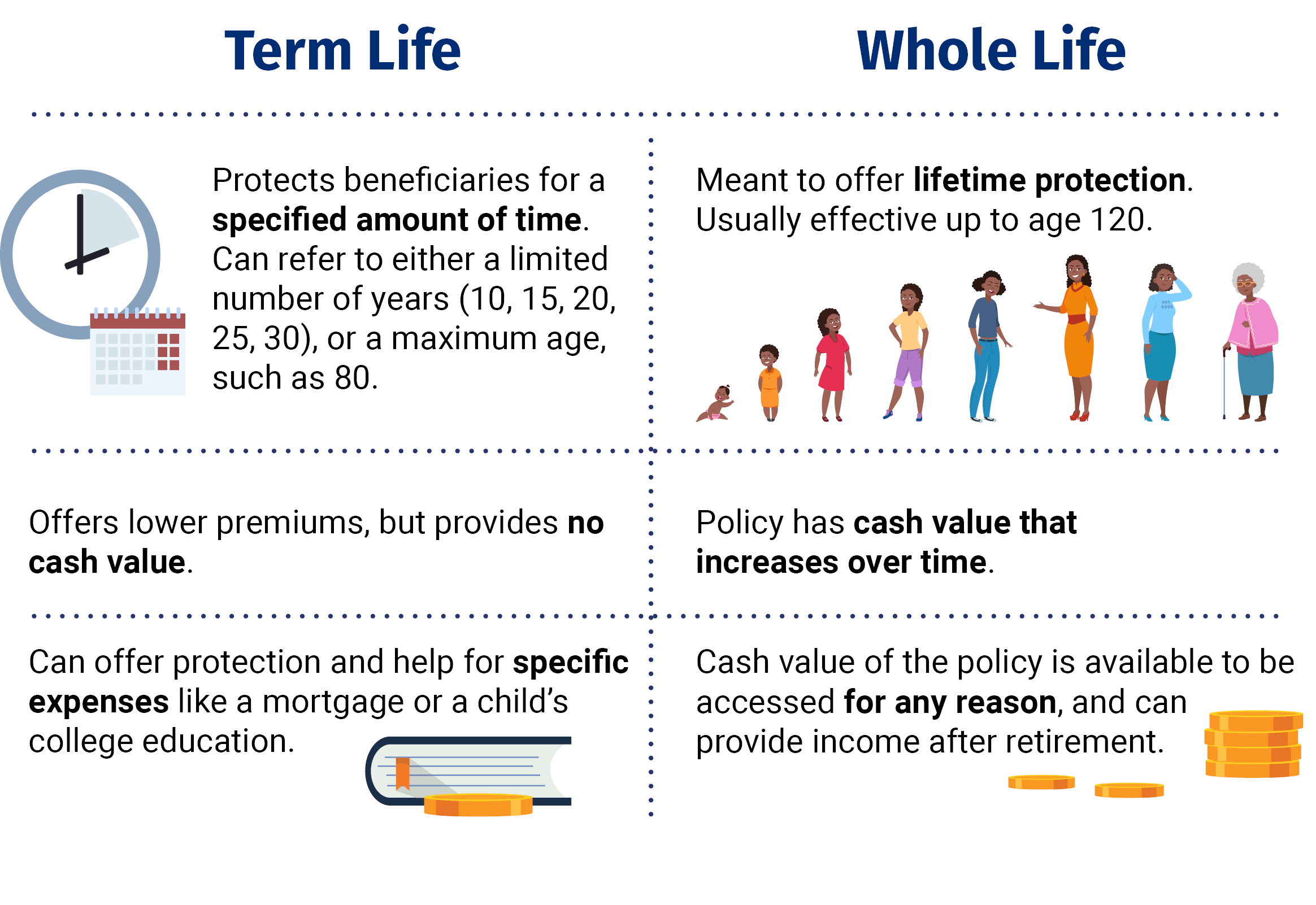

Term life plans are ideal for individuals that desire considerable protection at a low price. Individuals that own entire life insurance coverage pay much more in costs for less protection but have the safety of understanding they are protected for life.

The conversion cyclist must permit you to transform to any type of permanent plan the insurer supplies without restrictions - can you get term life insurance if you have cancer. The main functions of the motorcyclist are maintaining the original wellness ranking of the term plan upon conversion (even if you later have health problems or come to be uninsurable) and deciding when and just how much of the protection to transform

Of training course, overall costs will raise dramatically considering that whole life insurance is extra expensive than term life insurance policy. Medical problems that create throughout the term life period can not trigger costs to be raised.

Term life insurance is a reasonably economical way to offer a lump amount to your dependents if something takes place to you. It can be an excellent option if you are young and healthy and support a household. Entire life insurance coverage features significantly greater month-to-month costs. It is implied to offer insurance coverage for as lengthy as you live.

Term Life Insurance With Critical Illness Rider

It depends upon their age. Insurer set a maximum age limitation for term life insurance coverage plans. This is generally 80 to 90 years old yet might be greater or reduced depending on the business. The costs additionally climbs with age, so an individual aged 60 or 70 will pay substantially greater than a person years more youthful.

Term life is somewhat similar to cars and truck insurance policy. It's statistically unlikely that you'll require it, and the costs are cash away if you do not. However if the most awful happens, your household will obtain the advantages.

This policy layout is for the client that needs life insurance policy yet wish to have the capacity to select exactly how their cash money worth is invested. Variable policies are underwritten by National Life and distributed by Equity Providers, Inc., Registered Broker/Dealer Associate of National Life Insurance Policy Company, One National Life Drive, Montpelier, Vermont 05604.

For J.D. Power 2024 award info, check out Permanent life insurance policy develops cash worth that can be borrowed. Policy fundings accumulate rate of interest and overdue plan loans and interest will lower the survivor benefit and money value of the policy. The quantity of money value available will usually rely on the kind of permanent plan bought, the quantity of insurance coverage acquired, the length of time the plan has been in force and any outstanding plan fundings.

Which Of The Following Best Describes Term Life Insurance

Disclosures This is a general summary of protection. A total declaration of coverage is discovered just in the policy. For even more information on coverage, prices, constraints, and renewability, or to get insurance coverage, call your neighborhood State Farm representative. Insurance policies and/or connected cyclists and features may not be available in all states, and plan conditions may vary by state.

The major distinctions between the different kinds of term life policies on the marketplace relate to the length of the term and the insurance coverage amount they offer.Level term life insurance policy comes with both level costs and a degree survivor benefit, which indicates they stay the very same throughout the duration of the plan.

It can be renewed on an annual basis, yet costs will raise whenever you renew the policy.Increasing term life insurance coverage, likewise called a step-by-step term life insurance policy strategy, is a plan that includes a survivor benefit that raises with time. It's generally much more complex and expensive than degree term.Decreasing term life insurance policy features a payment that reduces gradually. Typical life insurance policy term sizes Term life insurance policy is affordable.

Despite the fact that 50 %of non-life insurance proprietors cite expense as a factor they don't have coverage, term life is among the least expensive type of life insurance policy. You can often obtain the coverage you require at a workable price. Term life is easy to take care of and understand. It offers coverage when you most need it. Term life supplies economic defense

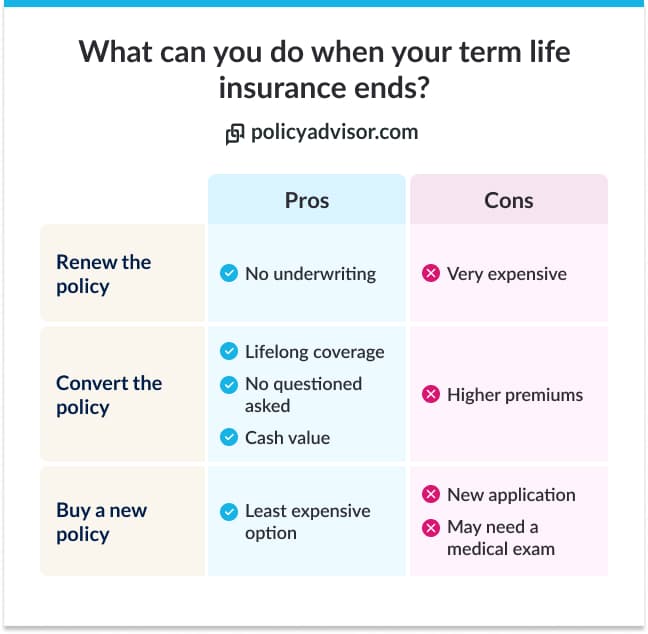

during the duration of your life when you have major monetary commitments to satisfy, like paying a mortgage or moneying your children's education. Term life insurance has an expiry date. At the end of the term, you'll need to buy a brand-new plan, restore it at a higher premium, or transform it right into irreversible life insurance policy if you still want protection. Rates may differ by insurance company, term, insurance coverage amount, health and wellness course, and state. Not all plans are readily available in all states. Price illustration legitimate since 10/01/2024. What aspects affect the cost of term life insurance policy? Your rates are identified by your age, gender, and wellness, as well as the protection amount and term length you pick. Term life is a good fit if you're trying to find an inexpensive life insurance plan that only lasts for a set amount of time. If you require permanent coverage or are taking into consideration life insurance coverage as an investment option, whole life may be a far better choice for you. The main distinctions in between term life and whole life are: The length of your protection: Term life lasts for a set amount of time and after that expires. Ordinary regular monthly entire life insurance policy rate is computed for non-smokers in a Preferred health category, obtaining a whole life insurance coverage policy paid up at age 100 provided by Policygenius from MassMutual. Prices may vary by insurance firm, term, insurance coverage amount, health class, and state. Not all plans are readily available in all states. Short-term life insurance policy's short-lived plan term can be an excellent choice for a couple of scenarios: You're waiting on authorization on a long-term policy. Your policy has a waitingperiod. You remain in between tasks. You intend to cover short-term obligations, such as a car loan. You're improving your wellness or way of living(such as stopping cigarette smoking)prior to getting a conventional life insurance coverage policy. Aflac uses various long-term life insurance coverage plans, consisting of whole life insurance policy, last cost insurance, and term life insurance policy. Start chatting with an agent today to learn more regarding Aflac's life insurance policy items and find the right choice for you. The most preferred kind is currently 20-year term. The majority of business will certainly not sell term insurance coverage to a candidate for a term that finishes previous his or her 80th birthday celebration . If a plan is"eco-friendly," that indicates it proceeds in pressure for an added term or terms, up to a defined age, also if the wellness of the insured (or other elements )would certainly cause him or her to be declined if she or he obtained a brand-new life insurance plan. So, premiums for 5-year renewable term can be level for 5 years, after that to a new price showing the new age of the insured, and more every five years. Some longer term plans will ensure that the premium will certainly notenhance throughout the term; others don't make that warranty, enabling the insurer to elevate the price during the plan's term. This means that the policy's proprietor can change it into a permanent kind of life insurance policy without extra proof of insurability. In many kinds of term insurance, including house owners and car insurance policy, if you haven't had an insurance claim under the policy by the time it ends, you get no reimbursement of the costs. Some term life insurance policy consumers have been unhappy at this end result, so some insurers have actually created term life with a"return of premium" feature. The premiums for the insurance with this function are commonly dramatically higher than for plans without it, and they usually call for that you keep the plan in pressure to its term otherwise you forfeit the return of costs advantage. Weding with children-Life insurance can assist your partner preserve your home, current lifestyle and supply for your youngsters's support. Solitary moms and dad and single income producer- Life insurance policy can assist a caregiver cover child care costs and various other living expenditures and meet prepare for your child's future education and learning. Weding without children- Life insurance coverage can provide the money to satisfy monetary obligations and help your spouse hold onto the properties and way of life you've both worked hard to attain. Yet you might have the choice to transform your term policy to long-term life insurance policy. Insurance coverage that shields somebody for a specified duration and pays a survivor benefit if the covered person passes away throughout that time. Like all life insurance policy plans, term protection aids preserve a family's monetary wellness in situation an enjoyed one passes away. What makes term insurance various, is that the guaranteed individual is covered for a detailsamount of time. Given that these policies do not give lifelong protection, they can be reasonably affordable when compared with an irreversible life insurance policy policy with the same amount of coverage. While the majority of term policies offer reliable, short-term protection, some are more adaptable than others. At New York City Life, our term plans supply an unique mix of functions that can aid if you come to be handicapped,2 become terminally ill,3 or merely wish to convert to a long-term life plan.4 Because term life insurance coverage offers temporary security, lots of people like to match the length of their policy with a crucial turning point, such as paying off a mortgage or seeing kids through college. Level premium term might be much more effective if you want the costs you pay to stay the same for 10, 15, or 20 years. As soon as that duration ends, the amount you spend for coverage will certainly increase each year. While both sorts of coverage can be effective, the choice to choose one over the other comes down to your specific demands. Given that no person knows what the future has in shop, it is essential to see to it your protection is dependable sufficient to fulfill today's needsand versatilesufficient to aid you plan for tomorrow's. Below are some crucial factors to bear in mind: When it comes to something this important, you'll intend to ensure the firm you utilize is monetarily sound and has a proven history of maintaining its pledges. Ask if there are attributes and advantages you can utilize in situation your requirements transform later on.

{kind=link}

Latest Posts

Las Vegas Term Life Insurance

$25,000 Term Life Insurance Policy

Increase Term Life Insurance